After working more than ten years at 11900 Wayzata Blvd., I have had no choice but to move my office. The new location is 10520 Wayzata Blvd. Suite 100, exactly a mile east of the old location. Moving day was October 17, 2023, but it has taken me a while to get settled in the new location and to update the address on my web site.

I say I had no choice because the 11900 building was being sold and is about to be town down. Apparently the new owners will be putting up a big apartment building. It seems a terrible shame to me. The old place was a quaint and comfortable place. I had a beautiful view of a pond where there was lots of wild life. Now here at the new place I have a view of a parking lot, a bill board and the I-394 freeway.

I have downsized and crammed my stuff into a space which is perhaps a third of what I had before. On the other hand, the new place has a massive waiting area, a play area for kids, a big conference room and a lunch room. I had none of those things at the old place. I’m getting used to it and starting to like it here.

Here’s some views of the outside and inside of the new place.

The most common type of bankruptcy is Chapter 7. It also tends to be the most desirable form of bankruptcy. Often it is referred to as “straight bankruptcy.” It is the type of bankruptcy where usually you can get rid of all your unsecured debt in just a few months with minimal cost. There is typically no payment plan, just relief from your debt.

The best way to qualify for a Chapter 7 is to have annual income below the median for your household size in your state. If your income is a bit higher than that, you might still be able to qualify by passing a means test; but the means test is not all that easy. I would prefer to have your income below the median if we are going to do a Chapter 7. If it is much above the median, I would probably suggest a Chapter 13.

Meidan Income – A Moving Target

The US Trustee’s office has just announced the biggest increase in Minnesota median incomes for bankruptcy purposes that I can remember seeing. I calculate that the increases are around 8% for all the household sizes between one and four. Since these increases are supposedly based on a six month period, they seem to be thinking that median incomes in Minnesota have been increasing by 16% on an annual basis. I find that hard to believe, but I won’t complain.

Most years the median income numbers are adjusted on April 1st and again on November 1st. Sometimes they all go up, sometimes they all go down, sometimes the ups and downs are mixed, and sometimes they don’t change at all. Every state is different and is assigned their own set of numbers.

Latest Numbers for Minnesota

Here’s the exact Minnesota numbers as of the recent update copied from my Chapter 7 page:

One person: $ 71,643

Two people: $ 90,946

Three people: $ 114,267

Four people: $ 141,324

Add $9,900 for each individual in excess of4

For a household of one the increase is $5,309 per year. For a household of two it’s a $6,739 per year increase. It’s $8,467 for a household of three, and $$10, 472 for a household of four. If you thought you didn’t qualify for a Chapter 7 before, take another look. These numbers could make a big difference.

Call or text me at 952-544-6356. We can set up a time for a free telephone consultation to talk over the details of your case.

After going for a couple of years without any of my Google reviews disappearing, I noticed that some were being removed starting November 15, 2022. As soon as I saw that a purge was in progress, I attempted to create a printout of all my reviews so I would have a record of what was disappearing. After the smoke settled, I went to review the printout. To my disappointment I saw that I had only captured the first couple lines of each review. Except for one, which I had already reproduced in full on my reviews page, the full text of the missing reviews was irretrievably gone. In total since November 15th I have lost nine reviews. What follows is a summary of the opening lines from eight of those reviews which I regret, except for one, is all I managed to preserve:

“Honestly, I don’t even know where to start with my review because there were so many incredible things about my experience with david Kelly. He came into my life during an extremely stressful time and managed to make me feel 90% better….”

“I definitely recommend anyone going through bankruptcy to go with Dave Kelly as their lawyer. He was professional in answering our questions and gave us a straightforward and thorough overview of the bankrupty process. ..”

I cannot express how satisfied and appreciative I am with the work of Dave. I started my online search for a great attorney and that is what I found. Dave’s website and YouTube videos were extremely helpful and very thorough. I have to say …..”

“David is a fantastic attorney. I had previously spoke with one of the larger firms in the area and did not like the way they moved the cases through very quickly and did not seem very personal to talk with. I felt like the larger firm only ….”

“Dave worked on my Chapter 13 bankruptcy with me. Filing for bankruptcy was one of the least comfortable things I’ve ever had to do. Bankruptcy was not something I came to lightly, I tried everything I could think of on my own before I …..”

“I was very lucky to get a lawyer that was Professional as well as someone who really cared about helping me out. I don’t believe that anyone wants to get a bankruptcy ever. It a little embarrassing, even in bad times that you can’t pay your ….”

“He was very professional and understanding of my situation. He was never pushy and always communicated very well. He never made me feel stupid or ashamed for filing and also made it very welcoming and comfortable. I’d highly recommend David to anyone who is considering filing. You won’t be disappointed.”

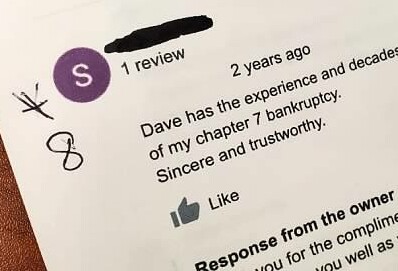

“David has the experience and decades of knowledge and proven results that got me through the process (with ease) of my chapter 7 bankruptcy.”

Quirky Standards and Requirements

Over the years I have lost well over 100 reviews which disappeared into Google’s bit bucket. Sadly they had all given me five stars. They can’t be retrieved. They are gone forever. Google seems to have very strict standards as to what reviews it allows to be posted. Some reviews are only there for a day or two before Google deletes them forever. Others can stay up for several months or even a couple of years before they disappear.

A couple of clients have given me five stars and posted simply “Thank you Dave.” Google didn’t like that and instantly removed their reviews, almost before I had a chance to notice. Another client kept having his review removed because he could not refrain from putting in too many superlatives about how great he thought I was. Webster defines “superlative” as an “exaggerated expression especially of praise.” What Google seems to be looking for in a review is a simple, toned down statement of what your experience was.

Most Common Reason Reviews Disappear

The reasons a Google review may disappear are certainly many. But the single most common reason seems to be lack of activity on the reviewer’s Google account. If you set up a Google account, use it to post a review, and then use that account for nothing else ever, the folks at Google will delete the account for inactivity after a year or two. Once the account is deleted, the reviews posted with that account are gone as well.

Only Speculation

I can only speculate as to why the reviews are gone. My comments about superlatives and everything else above is just a guess. I’ve been complaining to Google. All I get is an automated response that doesn’t really tell me anything. Words like heartless and cruel come to mind. All I can say is that it s painful to see this happening. These were people who I knew and cases I cared about.

This is the last in my series of articles about the top seven things that in my opinion you should avoid doing prior to filing a Chapter 7 or Chapter 13 bankruptcy. My list is not exclusive. There are lots of other things to be avoided. On one web page I saw a list of 33 things to avoid. All I am saying is that this list is my top seven. Others may disagree on my ranking of these.

Why is Debt Run-up Before Bankruptcy a Problem?

The reason you should avoid running up debt right before filing a bankruptcy is that doing so may result in an objection to your discharge from one of the creditors. Typically this would not be an objection to your entire bankruptcy case, but just an objection to the one particular debt owing to that particular creditor. The larger the debt and the closer to the filing date of the bankruptcy it was incurred, the greater the risk.

The creditor will review the account and use the history of the account to try and prove that you had no intent of paying the debt at the time you ran it up. If you had no intent to pay when you incurred the debt, the creditor can object on the grounds of false pretenses and fraud. The evidence that the creditor will use will usually be entirely circumstantial . Basically they put together their case and ask the judge “what’s this look like to you?” Often it can be pretty obvious, other times not.

Worse if for Luxury Good or Services

The creditor’s case is always stronger if the debt is for luxury goods and services, especially if the purchases spike right before the bankruptcy is filed. When somebody who hardly ever goes farther then Duluth suddenly decides they need a trip to Europe, it looks suspicious. Expensive restaurants, large purchases of alcohol, spas and pedicures don’t look so good either. On the opposite end of the spectrum is medical expense. People usually don’t have control of medical costs, and the medical providers almost never object.

What the Law Presumes

Ordinarily the creditor has the burden of proof when they file an objection to discharge. This means that the creditor has to prove their case and the debtor does not have to necessarily prove anything. The bankruptcy statute has two situations, however, where certain presumptions shift the burden of proof to the debtor. Here they are:

1. Any consumer debt for goods and services owed to a single creditor in excess of $725 incurred within 90 days of filing is presumed to be for luxury items. With the proper evidence in your favor, the presumption can be rebutted; but it’s best just to wait so you don’t have to go through a potential objection from the creditor.

2. Cash advances in excess of $1,000 made within 70 days of filing are presumed non-dischargeable. Again, if this has happened it may be best to wait until the time period has passed before filing.

What this Really Means

As a practical matter what does all this mean? In my opinion it means that you might not want to file a bankruptcy if you have run up a debt on any one account in an amount of more than 4 or5 thousand dollars in the past six months. If it’s much less than that, the creditor probably can’t afford to do an objection. If it’s much older than that, it’s might be too hard for the creditor to prove. This kind of recent debt runup doesn’t necessarily mean you should not file a bankruptcy. But it could be a good reason to delay the filing for a while.

Disclaimer

This post is for general information purposes only and is not legal advice. It does not create an attorney-client relationship. Consult the attorney or your choice about the details of your case.

Yesterday I received an email from the Minnesota Bankruptcy Court stating in part as follows:

If there is a lapse in appropriations after January 25, the U.S. Bankruptcy Court for the District of Minnesota will likely be operating with reduced staff focused on processing filings that directly affect the protection of human life and property, as required by the Anti-Deficiency Act. The court is still in the process of determining which activities can and cannot be performed during a shutdown, and will provide ongoing guidance as these determinations are made.

We anticipate that, during any shutdown:

CM/ECF will remain operational;

The BNC will continue to process and send notices in the ordinary course; and

PACER will remain operational and the PACER Service Center will provide ongoing support services.

In the coming days, we plan to set up an email box to which you can direct questions, concerns or comments about the shutdown. We will send out the email address with any additional updates as these become available.

I take this as meaning that for now I can continue with business as usual but that I better keep a close eye on things.

If you’ve been reading any of my musings, you know that when you file a Chapter 7 bankruptcy, ownership of all your stuff is temporarily and theoretically transferred to a trustee appointed by the court. I say “theoretically” because normally the trustee doesn’t get to keep any of it, or at least gets to keep very little. The reason why the trustee can’t keep your assets is that – with the help of somebody like me – you are going to claim all or most of your stuff as exempt. There are two sets of exemptions in Minnesota to choose from: the federal exemptions and the Minnesota state exemptions. The federal exemptions tend to be much better than the Minnesota state exemptions, except in one area: equity in a homestead. If you own your home and you have more than just a little equity in your home, the Minnesota state exemptions are for you.

Several of the Minnesota exemptions are indexed for inflation. The resulting increases are only applied every few years. 2018 was one of those years. The new indexed numbers went into effect on July 1st. For example: the household goods exemption increased from $10,300 to $10,800; for wedding rings the exemption increased from $2,817.50 to $2,940 in value; for life insurance proceeds it increased from $46,000 to $48,000; and the tools of the trade exemption went from $11,500 to $12,000. The most significant increase in my opinion was the homestead exemption which went from $390,000 of equity to $420,000 of equity.

For more info about exempting your property so the bankruptcy trustee can’t have it, look at my exemption page. For a rant about what’s wrong with the Minnesota state exemptions, please take a look at my post Minnesota State Exemptions Still Leaking Like a Sieve. You might also want to take a look at this video:

I want to say a few words about whether a debt owing to the Social Security Administration for overpayment of benefits can be discharged in a bankruptcy. Often it can be.

If you have received Social Security you know that several factors, many of them beyond your control, can affect whether you are eligible and for how much. This is especially true of disability benefits. A change in status can end your eligibility or reduce the amount. It’s all very complicated and hard to understand – especially if you are ill.

The Social Security Administration is a big and cumbersome organization that makes lots of mistakes. Lots of times they pay benefits when they are not supposed to. Often this happens because they can be very slow in processing information they receive from beneficiaries. The impression I have is that most beneficiaries are very careful about complying with requirements that they report any change in their circumstances. If you report the change and the benefits keep coming, most people would assume that the change didn’t make a difference. Later, however, you may be shocked to receive a nasty letter from the Social Security Administration. The letter claims that you have been overpaid and demands repayment.

Suddenly you have a very large debt to a federal government agency. Nobody is more powerful. They might start withholding from the benefits you are still eligible for; they might seize your tax refunds; or they might even start garnishing your wages. Most people assume that like the usual student loans and taxes, there is no way to make this go away. This is what I assumed too the first time someone came to my office with one of these letters.

I was surprised to learn when I did a little research that many if not most of these Social Security overpayment claims can be discharged in bankruptcy. When a debt like this is listed in a bankruptcy, it is going to be discharged unless the Social Security Administration successfully objects. In order to figure out whether to expect an objection, it is helpful to check Social Security policies as published in their on line Program Operations Manual. The guidelines as to when such an objection should be filed are in GN 02215.196 of the manual. They will object if they believe they can prove that the overpayment was a result of fraud or misrepresentation.

They use a three part test to define what they mean by misrepresentation. There must have been 1) an overpayment caused by false representation, 2) made with the intent to deceive and 3) upon which the Social Security Administration relied to it’s detriment.

The typical person I see in my office who with one of these overpayment letters isn’t anywhere close to satisfying the above test. This person hasn’t told any lies and certainly wan’t trying to deceive anybody. There was no intent to cheat the government out of anything. It was more a matter of just stumbling into the situation. If this is where you find yourself, you might want to give me a call. The chances that a bankruptcy can make the whole problem just go away are very good.

When you file a Chapter 7 bankruptcy, ownership of all your assets all the way down to your socks passes to a trustee appointed by the court. The only way to avoid losing your shirt and most everything else you own is to claim the assets as exempt. If you qualify to use the federal exemptions, it is very likely that everything you own will be exempt and you will keep all your assets. That’s the result I always want to see – my client gets rid of his or her debts but keeps all his or her stuff.

The only problem with the federal exemption list is that it has a low number for the amount of homestead equity which can be exempted. If someone has more equity than can be protected by the federal exemptions, the only other choice is to use the state exemptions. The Minnesota state exemptions will protect up to $$390,000 of equity in a homestead, but other than that those exemptions leave a lot to be desired. They are hopelessly out of date in many respects.

For example, the only electronics clearly allowed as being exempt are a radio, a phonograph and television receivers. Notoriously, computers are not exempt. Neither are cell phones, tablets, game machines, printers, monitors or any other device that isn’t a TV, radio or phonograph.

There’s no exemption for jewelry, unless it’s a wedding ring that was actually present at the wedding ceremony. There’s no exemption for guns, sporting goods such as bicycles or exercise equipment, or collectibles of any kind. Household furnishings, clothing and appliances are exempt, but a riding lawn mower is not considered to be an appliance. Money in your checking account or savings account is not exempt unless it can be traced to a pay check from employment which was deposited within the last 20 days. There’s no exemption for any kind of a tax refund which may be owing or which may have accumulated as of the date of filing the bankruptcy. Bankruptcy trustees routinely present my clients with a form which signs over their tax refunds.

Several weeks ago two bills were introduced at the state legislature in St. Paul to try and correct some of this. One of them added exemptions for the following, all of which currently are absent from the exemption list:

Computers, tablets, printers and cell phones as part of the household goods exemption

Jewelry up to a value of $2,817.50 – replacing the existing wedding ring exemption

A new section exempting $3,000 of tools, snow removal equipment and lawnmowers

A wild card exemption which could be used for up to a $1,250 value of property not fitting into any other exemption; and

Health savings accounts (HSA) and medial savings accounts up to a value of $6,500.

When I heard last week that the legislature had passed an amendment to the exemption statute, I got quite excited. I thought it must be the bill I just described above. I was quite disappointed to learn that it was another bill which only added one provision: an exemption for health savings accounts and medical savings accounts up to a value of $25,000. It’s nice that the amount of the exemption is so high, but I almost never see anyone with an HSA which has any more than a few hundred dollars in it.

So except for the new exemption for the HSAs, we are still stuck with all the same old problems with the Minnesota state exemptions. Oh well, at least the antique radio in my office is exempt.

In 2016 when I was first contacted by Expertise.com I was very skeptical, as evidenced by what I posted here at that time. I have received all sorts of scam emails from one outfit or another which try to get attention by announcing that they are giving me some sort of award. Often all they are trying to do is sell me a meaningless plaque to hang on my wall. Sometimes they are offering to list me in some sort of Who’s Who book, for a fee of course. Other times they are fishing for personal information such as a bank account number or a password.

Another reason for my skepticism is that after my typical Minnesota upbringing, I find it very hard to accept praise or gratitude of any kind. My default response to anybody saying anything nice about me is to respond by saying it was no big deal or by minimizing it in some way. When someone says “thank you” to me, instead of just saying “you’re welcome” I tend to launch into some long explanation as to why I don’t deserve to be thanked. Having become aware of this, I have actually been practicing saying “you’re welcome,” and it’s not easy.

After passage of some time and after I’ve done some investigation, I have come to the conclusion that Expertise.com is legitimate. They made a serious effort to take a look at the bankruptcy lawyers in the Minneapolis area and rate them based on reputation, credibility, experience, availability and professionalism. To them I wish to say thank you and I’m honored.

I recently posted on Google Plus about how certain things tend to be toxic to a possible bankruptcy. The most common one I see is a Harley Davidson. Other items in this category would include boats and horses, especially if they are fancy and not paid for. This statement resulted in questions being asked about exactly what I meant. If the problem is that a Harley, a boat or a horse are assets which would be lost in a Chapter 7 bankruptcy, then wouldn’t it be better for them to not be paid for. If they weren’t paid for, after all, they wouldn’t be much of an asset.

My answer was that such items make a bankruptcy difficult whether paid for or not. If they are paid for, they are assets that very likely would be lost in a Chapter 7 or would increase the required payments in a Chapter 13.

If they are not paid for, you have a situation where the Debtor will want to tell the bankruptcy trustee that he or she can’t afford to pay debts, except that somehow they CAN afford to keep paying for the Harley, the boat or the horses. This does not play well. The only thing to do if they really need the bankruptcy is to sell or surrender before filing, or state in the bankruptcy petition an intention to surrender the items after the case is filed.

Many have been the times when I have had a potential client disappear never to be heard from again when I said that the Harley has to go. There’s a whole subculture where any kind of misery is preferable to giving up the Harley. Boats are usually a bit easier to let go, but horses are also very hard to give up.

One exception might be a case with a 100% Chapter 13 plan. That would be a plan where 100% or the unsecured debts are to be paid. Since the bankruptcy trustee can’t ask for more than 100%, the Debtor would have more wiggle room when it came to something like keeping a motorcycle. Even then the trustee would not like it, but more than likely the trustee could not prevent it. I see very few cases where the payout is 100%. Most people who can afford to do that don’t need a bankruptcy.

This post is for general information purposes only, is not legal advice and does not create an attorney-client relationship. I am a Debt Relief Agency. I help people file for relief under the federal bankruptcy code.